As any corporate development officer knows, it takes a village to do a deal. Corporate development teams are small by design and need to leverage a large volume of resources to execute a transaction. It’s not unusual to see a team that is 90 or 95% external to corporate development. The leader of the deal process needs to construct a team that brings the right skills,expertise, and capacity to execute the deal effectively. Leveraging vendors effectively can increase the quality, speed, and capacity of a deal making company. But failing to effectively integrate, the team can have the reverse effect, slowing the deal process, reducing quality, and creating dangerous gaps in work. In this article, we will discuss how to effectively use vendors in an M&A deal process.

Internal vs External Vendors

It takes a village to raise a child, as the old adage goes. And every corporate development officer knows the M&A version: it takes a village to do a deal.

Corporate development teams are small by design and need to leverage a large volume of resources. It's not unusual to see a team that’s 90 or 95% external to corporate development. The leader of the deal process needs to assemble a team with the right skills, expertise, and capacity to execute the deal effectively.

Successfully leveraging vendors can increase the quality, speed, and capacity of a deal-making company. But if the team fails to integrate, it can have the reverse effect: slowing the deal process, reducing quality, and creating dangerous gaps in work.

In this article, we’ll discuss how to properly use vendors in an M&A deal process.

Choosing where to use vendors is a critical element and force multiplier for your team. Outside vendors are often seen as a gap-filling resource, but we know better. Lawyers and investment bankers have long been viewed as standard parts of the deal process because they bring specific expertise not found in-house, and the same mindset should be applied to other vendors.

A blended team of corporate development, internal operators, and external vendor experts usually yields the most effective and efficient team when properly structured and integrated. Creating a standard process and playbook for deploying these resources often makes the discussion with business leaders easier.

How to Map Vendors Across the M&A Deal Process

Deals require the deployment of a range of different expertise against different topics. Since investment banking and legal topics are more commonly understood, I'll leave them out of this analysis.

These include, but are not limited to:

Note: This list of topics is far from exhaustive, and the topics often 'cross streams.' For example, pricing analysis combines market/customer insights with financial analysis. For corporate acquirers, the integration path is overlaid onto all of these topics, multiplying the complexity of evaluation (i.e., not just the quality of the target codebase but also how easily it can be integrated with the acquirer's codebase). For many of these topics (particularly those in bold), there is a natural use case for outside vendors to bring unique expertise and methodologies to the process.

Since deals move quickly, it’s worth identifying and vetting vendors in advance of a live deal. In the heat of the LOI process, you don't want to be burdened with vendor due diligence and reference calls. You also want ample time to map out how the vendors will integrate into your deal team. Having a stable list of vendors ready for use will make deploying them at 'deal speed' much easier.

How to Evaluate the ROI of M&A Vendors

Vendors cost money and may initially be seen as an incremental (and potentially unneeded) expense. But this is usually an incorrect and short-sighted assumption. Vendors need to be viewed as both a replacement for internal resources that have a better, higher-value use (for example, taking a salesperson offline to review a target pipeline methodology) and a more effective tool for managing much larger risks and driving much bigger opportunities.

Vendors' costs should be viewed in the context of the risk mitigation and value creation they bring. For a $50M acquisition, even a modest improvement in integration speed, go-to-market timeline, employee retention, clear development roadmaps, etc., can pay for a lot of vendor resources.

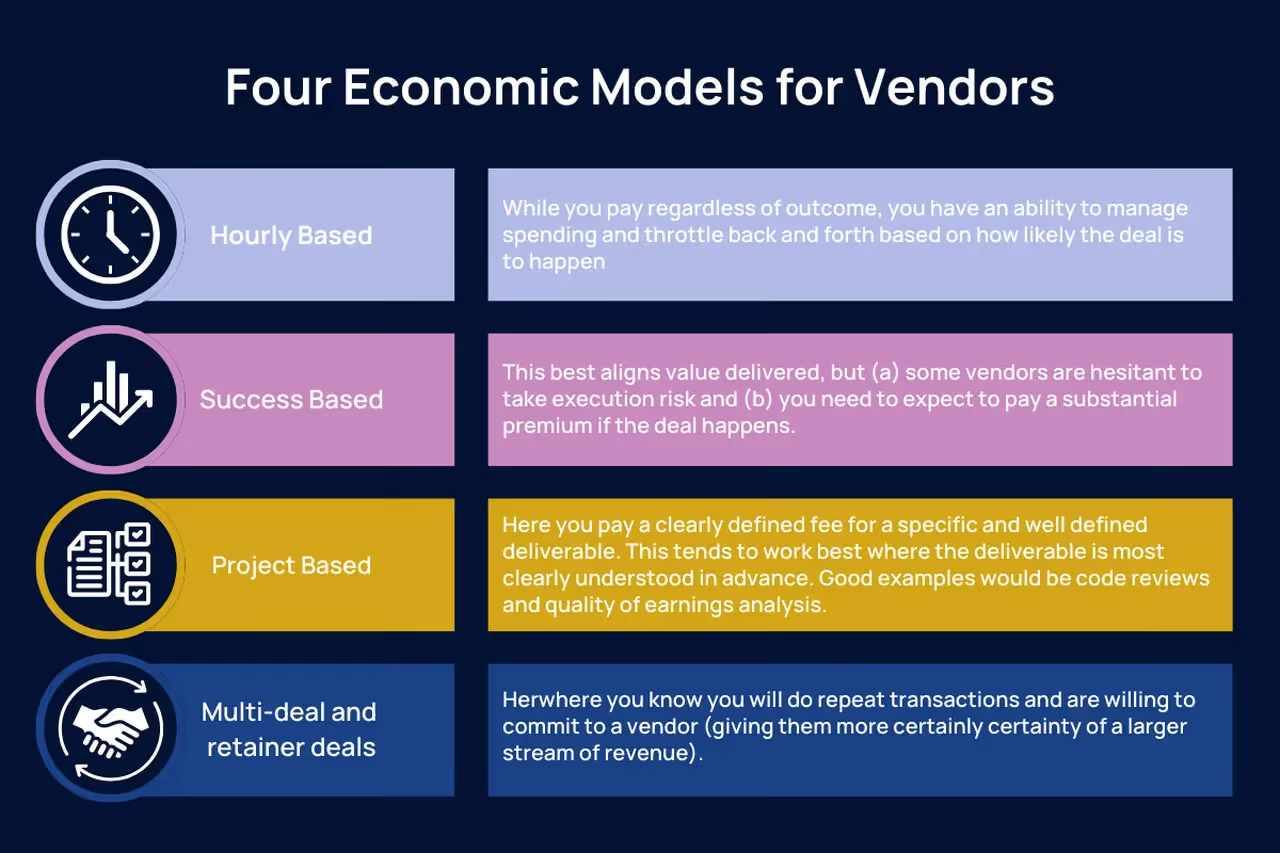

There are also a number of different economic models for vendors that can help align incentives and impact.

1. Hourly based

While you pay regardless of the outcome, you can manage spending and throttle back and forth based on how likely the deal is to close.

2. Success-based

This best aligns with the value delivered, but (a) some vendors are hesitant to take execution risk, and (b) you need to expect to pay a substantial premium if the deal happens.

3. Project-based

Here, you pay a clearly defined fee for a specific and well-defined deliverable. This tends to work best where the deliverable is most clearly understood in advance. Good examples include code reviews and quality-of-earnings analysis.

4. Multi-deal and retainer deals

Where you know you will do repeat transactions and are willing to commit to a vendor (giving them more certainty of a larger stream of revenue).

How to Evaluate M&A Vendors Before a Deal

The right vendor is not just an expert but also a fit for the size/type of deals you do. When building your vendor stable, consider a range of factors beyond their expertise.

You should consider:

1. Cost

Cheapest is not always best, but you want a vendor whose pricing is appropriate for your deal size, industry, and the type of work you need them to do. The right vendor to conduct a deep analysis of AI tech for multi-billion-dollar deals is not, in most cases, the right vendor to conduct a code review of a small traditional SaaS business.

2. Expertise

Your vendor should not only have expertise in the topic but also, ideally, in the industry sector in which you and your targets operate. Sales ops are radically different in consumer products and biotech businesses.

3. Deal experience

Not all vendors are experienced with the type of analysis needed for an M&A transaction and the pace at which they run. They also need to be comfortable with the level of 'on-the-fly' coordination required between their work and other parts of the deal process.

4. Capacity

Given the pace and sudden acceleration of deals, it’s important to work with vendors who can scale quickly when timelines compress. An argument can be made for choosing vendors that are small enough to prioritize your work yet large enough to have sufficient resources.

5. Synergies of recurrence

Choosing vendors that understand your process, needs, and organization will also streamline their work and improve integration with your team.

How to Integrate Vendors Into the M&A Deal Team

While a vendor's work is valuable in isolation, most of its value will come from its integration and coordination with your team and other workstreams. Some keys to achieving that broader value include:

1. Preparation and clear expectations

- Set clear expectations for the vendor's workflow and timing of deliverables.

- Make sure the vendor (particularly if this is your first deal together) understands not only their work but your process, priorities, culture, etc. This includes understanding your business goals in general and for this deal. For example, if you are planning to scrap the target brand, a market insights vendor should not spend time evaluating its strength.

- Allow time for prep calls and clear alignment before the work launches.

- Internal and external team members must be connected and allowed to communicate directly.

2. Over-communication

- Avoid silo thinking by having clear and regular communications between different workstreams and make sure the vendor is part of those (not limited to 'internal teams').

- Insist that the vendor shares work in progress rather than waiting for a finished product. This may be uncomfortable for vendors used to owning more of an end-to-end project.

3. Agile process

Vendors must be able to adjust their plans based on new information during the diligence and integration planning process, which may affect the use of project-based pricing or require addenda.

4. Partnering up teams

When a topic is covered by multiple teams (BU internal, CD team, Vendor), it’s important to proactively create a topic team. Otherwise, there will be a tendency for each group to work in isolation. For example, the QofE is much more valuable if it also informs the financial projections. This is similar to the challenge of getting integration and diligence teams to feed information back and forth.

It's important to create points of integration/collaboration/communication when multiple teams are covering the same topic to avoid working in isolation. Integration and communication between teams like QofE and financial projections is crucial.

Leveraging and integrating vendors into your deal process effectively can be key to providing not only key resources but also higher-quality results, from identifying risks to developing a more effective integration plan.

FAQ: Using Vendors in M&A

How early in the deal process should you bring in outside vendors? Before the deal is live. Vetting vendors mid-process costs time you don't have. Build a list of vetted vendors by workstream before a deal surfaces so you can move at deal speed when it does.

What's the risk of using the same vendor across multiple deals? Familiarity with your process helps, but leaning too heavily on one vendor creates a problem if they're at capacity when a deal accelerates. Keep two to three vetted options per workstream so you're not scrambling.

How do you manage confidentiality when working with external M&A vendors? NDAs are table stakes. Beyond that, vendors should only see what's relevant to their workstream. Keeping access compartmentalized, especially before LOI, limits exposure if something leaks before it should.

What's the difference between a vendor and a Certified Advisor in M&A? A vendor delivers a defined output: a code review, a quality-of-earnings analysis, or a market assessment. A Certified Advisor brings deal-stage judgment: someone who has run the same situation before and can help a team navigate it, not just complete a task. Buyer-Led M&A™ Certified Advisors are matched by sector, region, function, and deal stage through Certified Advisor on Demand.

How do you set up a vendor bench before a deal is live? Map your standard deal workstreams and identify where your internal team consistently runs thin. For each gap, vet two to three vendors and run reference calls when you're not under pressure. Keep the list in your deal playbook so it's accessible when a process moves fast.