.avif)

Mergers and acquisitions (M&A) refers to the process of combining two or more companies through transactions such as acquisitions, mergers, divestitures, joint ventures, and strategic alliances. Companies use M&A to accelerate growth, enter new markets, acquire talent or technology, and strengthen competitive positioning faster than organic growth allows.

When a deal gets announced, what you see is a headline and a number. What you don't see is the strategy that led to it — the months of diligence, the late-night negotiations, and the integration work that actually determines whether the deal was worth doing. After a decade of conversations with the practitioners who lead these transactions, one truth holds: what separates successful M&A from failed M&A is almost never the financial model. It's everything that happens before and after it.

This guide covers the fundamentals — what M&A means, how mergers differ from acquisitions, the types of deals, why companies pursue them, and what the process looks like from the inside.

In this guide:

- What Is the Difference Between a Merger and an Acquisition?

- What Are the Types of M&A Transactions?

- Why Do Companies Pursue M&A?

- How Does the M&A Process Work?

- What's the Difference Between Proactive and Reactive Acquirers?

- What Are Joint Ventures, Strategic Alliances, and Partnerships?

- Frequently Asked Questions

What Is the Difference Between a Merger and an Acquisition?

The terms get used interchangeably — but they describe two different structures.

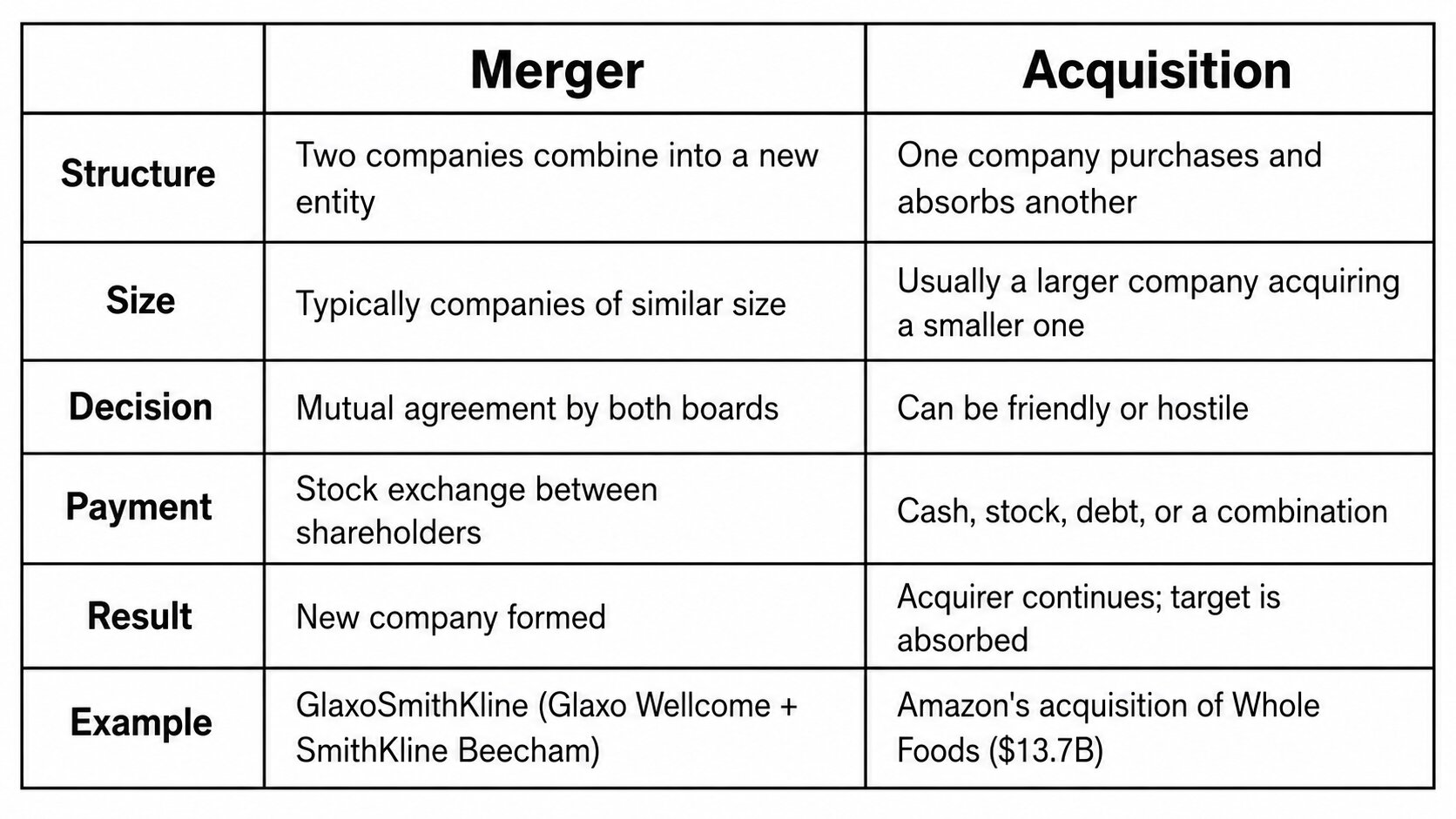

A merger occurs when two companies of roughly equal size agree to combine into a single new entity. Both companies cease to exist in their original form, and shareholders on both sides receive shares in the newly created company. Mergers are consensual — both boards of directors must approve.

An acquisition occurs when one company purchases another and takes ownership. The target either becomes a subsidiary of the acquirer or ceases to exist as a separate entity. Acquisitions can be friendly — where both sides agree — or hostile, where the buyer bypasses the board and takes the offer directly to shareholders.

In practice, the line blurs constantly. Many deals called mergers are functionally acquisitions — one company's leadership, culture, and systems end up running the combined entity. The real distinction is about deal structure and power dynamics, not what appears in the press release.

Acquisitions are also structured in different ways:

- Stock sale: The buyer purchases the target's shares, taking ownership of the full business — assets and liabilities included.

- Asset sale: The buyer purchases specific assets only — IP, equipment, a product line — without taking on the full entity or its obligations.

- Divestiture (carve-out): A company sells off a portion of its own business, usually to refocus on core operations or raise capital.

What Are the Types of M&A Transactions?

M&A transactions are generally categorized by the strategic relationship between the companies involved.

Horizontal M&A combines two direct competitors in the same industry. The goal is typically to increase market share, eliminate overlap, or achieve economies of scale. These deals attract the most regulatory scrutiny because they reduce competition in a market.

Vertical M&A involves acquiring a company in your own supply chain — either a supplier (backward integration) or a distributor or customer (forward integration). The goal is to control more of the value chain.

Conglomerate M&A brings together companies from unrelated industries. The primary driver is diversification — spreading risk across different markets.

Concentric (congeneric) M&A involves companies that aren't direct competitors but serve the same customer base or adjacent markets. The goal is to expand the product portfolio and cross-sell to an overlapping audience.

Market extension M&A happens when two companies sell the same product in different geographic markets. The acquisition is a shortcut to geographic expansion.

Product extension M&A combines companies that sell different but related products to the same market — broadening the range of offerings to existing customers.

One pattern holds across all deal types: the category of M&A matters far less than the strategic clarity behind it. The deals that fail aren't failures because of deal type — they fail because the buyer couldn't clearly articulate why the acquisition made their company better.

Why Do Companies Pursue M&A?

At its core, M&A is a growth tool. The logic: the combined company should be worth more than the two businesses operating independently. That concept is called a synergy — and it's the financial justification behind most deals.

What Are Synergies in M&A?

Synergies come in two forms:

- Cost synergies: The combined company reduces expenses by eliminating redundancies, negotiating better supplier terms at scale, or consolidating systems and facilities.

- Revenue synergies: The combined company generates more sales than either could alone — through cross-selling, new market access, or bundled product offerings.

Strategic Reasons Companies Pursue Deals

Beyond the numbers, companies do M&A for specific strategic reasons:

- Market expansion — entering a new geography or customer segment faster than organic growth allows

- Product diversification — adding capabilities to the portfolio (Apple's acquisition of Beats in 2014 added an established hardware brand and a streaming platform overnight)

- Capability acquisition — buying talent, technology, or IP that would take years and significant capital to build internally

- Defensive positioning — acquiring a competitor before it matures into a larger threat (Meta's acquisition of Instagram in 2012)

- Economies of scale — spreading fixed costs across a larger revenue base to drive down per-unit costs

When M&A Goes Wrong

Not every deal creates value. Research from Harvard Business Review and McKinsey consistently shows that between 70% and 90% of acquisitions fail to achieve their intended strategic or financial objectives.

The reasons are usually some combination of overpaying, underestimating integration complexity, cultural misalignment, and weak strategic fit. The 2001 AOL–Time Warner merger — valued at roughly $350 billion — remains the most studied failure in corporate M&A history. Cultural clashes and fundamentally incompatible business models erased most of the combined entity's value within years of close.

Strategic clarity and integration discipline are what determine whether a deal delivers. Without both, the financial model is just a story told before the work starts.

How Does the M&A Process Work?

Every deal is different, but most transactions follow a recognizable sequence:

- Strategy development — Define why you want to do a deal and what kind of target creates the most strategic value.

- Target identification and sourcing — Build a pipeline of candidates through investment bankers, industry contacts, or an internal corporate development team.

- Initial approach and evaluation — Make contact, exchange preliminary information, and determine whether the opportunity warrants deeper exploration.

- Due diligence — A thorough investigation of the target's financials, operations, legal obligations, customers, technology, and culture. This is where assumptions get tested against reality.

- Valuation and deal structuring — Determine what the target is worth, how the deal will be financed, and how the transaction will be structured.

- Negotiation and letter of intent (LOI) — Negotiate price, key terms, and conditions. The LOI sets the framework before a binding agreement is signed.

- Definitive agreement and closing — Sign the purchase agreement, satisfy regulatory and closing conditions, and transfer ownership.

- Post-merger integration — The work of combining the two businesses: systems, teams, culture, processes. This is where deals are ultimately won or lost.

That last step is the one underestimated most consistently. Across 400+ conversations on the M&A Science Podcast, integration is the single topic that comes up most often — because it's where value is either created or destroyed. The deal is just the beginning.

What's the Difference Between Proactive and Reactive Acquirers?

Not every company approaches M&A the same way.

Proactive acquirers treat M&A as a core part of their growth strategy. They maintain a pipeline of targets, run dedicated corporate development teams, and evaluate the market continuously. Large public companies with strong balance sheets typically operate this way.

Reactive acquirers move when an opportunity lands in front of them — a competitor becomes available, a founder decides to sell, or a new technology changes the competitive landscape. They may not have a standing M&A function, but they recognize strategic fit when they see it.

The best acquirers are proactive in strategy and disciplined in execution. Knowing when to walk away is as important as knowing when to move. Defining deal thesis and kill criteria before you start is what separates repeatable M&A programs from one-off bets.

What Are Joint Ventures, Strategic Alliances, and Partnerships?

M&A isn't the only way to grow through external relationships. When neither party wants to give up ownership, other structures allow collaboration without combination.

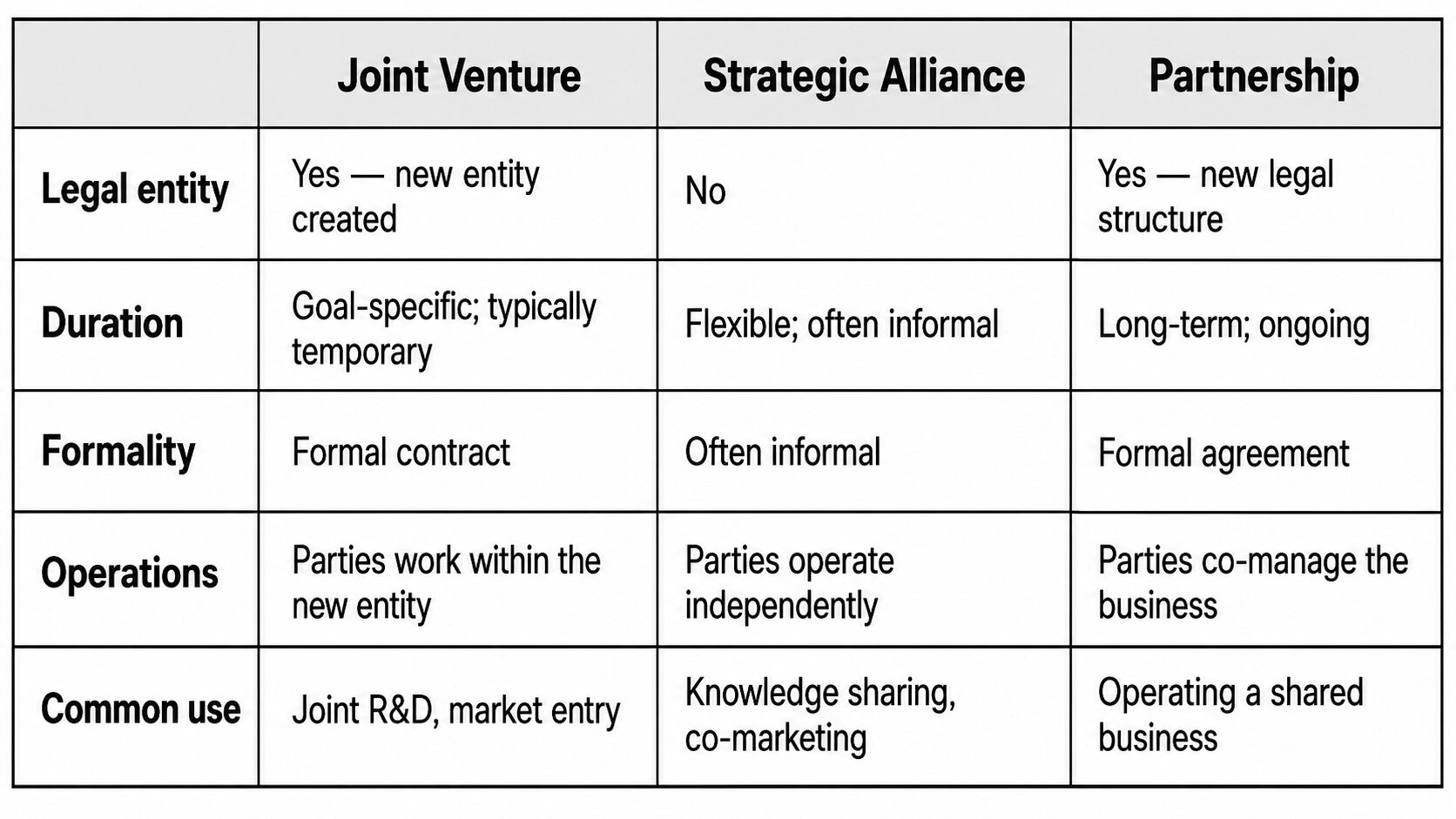

Joint Ventures

A joint venture is a formal agreement between two or more parties to create a new, separate entity for a specific purpose. That entity operates independently from the parent companies and typically dissolves once its objective is achieved.

In 2011, Ford and Toyota formed a joint venture to co-develop hybrid systems for light trucks. Toyota brought its leadership in hybrid technology; Ford brought its dominance in the pickup market. Both companies eventually integrated the resulting technology into their own product lines independently.

Joint ventures make sense when companies want to share the cost and risk of entering a new market or building a new capability — without the commitment of a full merger.

Strategic Alliances

A strategic alliance is a collaborative agreement between two companies that remain fully independent. No new entity is created — the parties agree to work together on a shared initiative while continuing to operate on their own. These can be as formal as a multi-year contract or as informal as a handshake agreement.

Partnerships

A partnership is a formal legal structure where two or more parties agree to operate a business together on an ongoing basis. Unlike joint ventures (goal-specific and temporary) and alliances (often informal), partnerships are long-term legal arrangements governed by a partnership agreement. Partners share profits, losses, and management according to the terms they set.

Frequently Asked Questions

What is the purpose of mergers and acquisitions? The primary purpose of M&A is to create value by combining two businesses — through cost savings, revenue growth, market expansion, or technology and talent acquisition. Companies pursue M&A when the combined entity is expected to be worth more than the two businesses operating independently.

What is the difference between a merger and an acquisition? In a merger, two companies of roughly equal size combine into a new entity — both dissolve in their original form. In an acquisition, one company purchases another and absorbs it. The acquired company either becomes a subsidiary or ceases to exist separately. Many deals called mergers function as acquisitions in practice.

What is a hostile takeover? A hostile takeover is an acquisition where the buyer bypasses the target company's board and takes the offer directly to shareholders — either through a tender offer or by attempting to replace the board to force approval. The target's management opposes the deal; the buyer proceeds anyway.

What are synergies in M&A? Synergies are the additional value created when two companies combine. Cost synergies reduce expenses through economies of scale, eliminated redundancies, or consolidated systems. Revenue synergies increase sales through cross-selling, expanded market access, or bundled offerings. Synergy projections are a core part of deal valuation — and among the most frequently overstated assumptions in any deal model.

What is due diligence in M&A? Due diligence is the comprehensive investigation a buyer conducts before committing to an acquisition. It covers the target's financials, legal obligations, contracts, customer relationships, technology, operations, and culture — the goal being to verify the seller's representations and surface any material risks before the deal closes.

How long does an M&A transaction typically take? It varies significantly. A straightforward private acquisition might close in 2–3 months. A large public-company merger with regulatory review can take 6 to 18 months or longer. Timeline is also shaped by the complexity of diligence and the number of regulatory jurisdictions involved.

What is an example of a successful acquisition? Disney's acquisition of Pixar in 2006 for $7.4 billion is one of the most studied successes in M&A. Disney gained Pixar's creative talent and technology pipeline; Pixar gained Disney's distribution and marketing infrastructure. The combined entity produced some of the highest-grossing animated films ever made.

What is the most common reason M&A deals fail? The most consistent failure drivers are overpaying for the target, underestimating integration complexity, cultural misalignment, and weak strategic fit from the outset. Most integration problems are visible during diligence — they get ignored until after close.